Senior Editor

By the time you read this, you’ll either be getting ready to elect a president, or you’ve recently cast your ballot. Once that happens, we still won’t know for certain where business will be going during the next few years, but at least one unknown, the next president, will become known.

The year has been full of unknowns. Where is Europe headed? How about China? How about that fiscal cliff we’re supposed to be on the edge of? How about our future workforce? Where will the next press brake guru come from, the next welder, or the next machine programmer?

Despite the uncertainties, fabricators are opening their wallets for capital equipment. According to the soon-to-be released 2013 Capital Spending Forecast, published by the Fabricators & Manufacturers Association, projected spending for U.S. metal fabricators climbed by 4 percent over last year. The total amount—more than $2.2 billion, a number extrapolated from a statistical sample of U.S. fabricators—is just shy of where readers projected spending to be before the recession. Business owners continue to worry, but they know if they sit still, they’ll be left behind.

This year’s total spending projection may be even more significant because financing has changed since the heady days before the financial crash, yet growth continues unabated. FMA’s 2012 Financial Ratios & Operational Benchmarking Survey shows how financially strong some companies are today. The weaker companies have been sold or shut their doors, and the strong firms continue to get stronger. They know they need to invest in the business to ensure they maintain their strong position before the next dip in the business cycle. These players are in positions to buy.

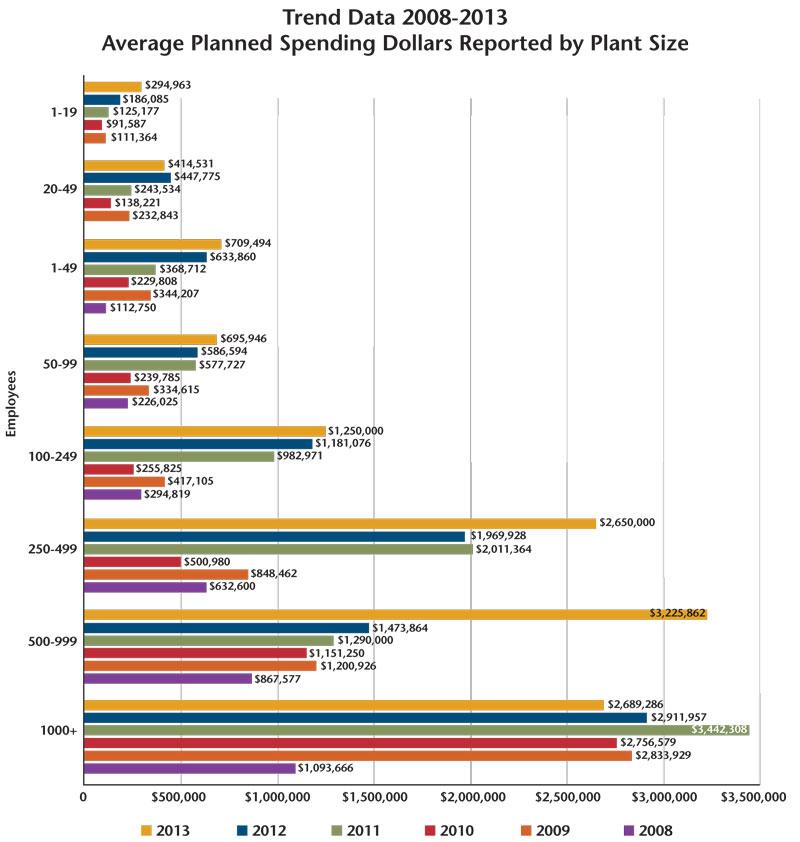

Small companies always made up a significant part of this business. Although individual company spending is small relative to larger players, taken together, fabricators with fewer than 50 employees account for a quarter of all equipment spending nationwide. And spending at the smallest companies continues to trend upward. Companies with 1 to 19 employees predict 2013 spending will be more than 200 percent more than forecast for 2010. (Those projections were understandably low, considering they were made in 2009, which for many was the trough of the recession.)

Not every fabricator is spending so aggressively. The largest fabricators in the survey, with 1,000 employees or more, decreased spending predictions by 7 percent, on average. And for the first time since the survey has tracked these numbers, predicted spending by slightly smaller companies, though still large—those with 500 to 999 employees—shot past their larger cousins. In this category, predicted spending has more than doubled from last year and more than tripled since the recession. Fabricators with 250-499 employees also increased their projected spending significantly, 34 percent over last year (see Figure 1).

All this may reflect a trend of consolidation, at least in some local markets. During the recession and the ensuing recovery, stronger companies took market share away from the weaker players. Consider comments Mike Jacobs made at The FABRICATOR’s Leadership Summit earlier this year. Jacobs is vice president of strategic sourcing, operations, and engineering for Rockwell Automation in Milwaukee. Globally, Rockwell has more than 5,000 suppliers. “We are aggressively reducing that number,” he said. “We think it’s in our best interest to work with a much smaller group of high-performance suppliers.”

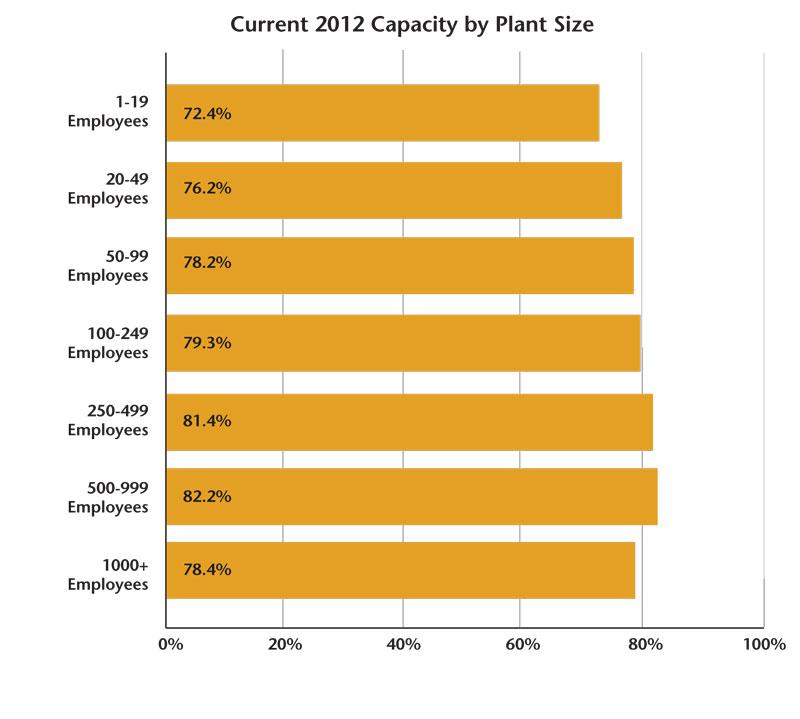

More work is being sent to fewer companies, and this may help explain current spending trends in capital equipment. Companies with 500 to 999 employees not only have the highest spending projections, but they’re also operating at the highest capacity utilization levels.

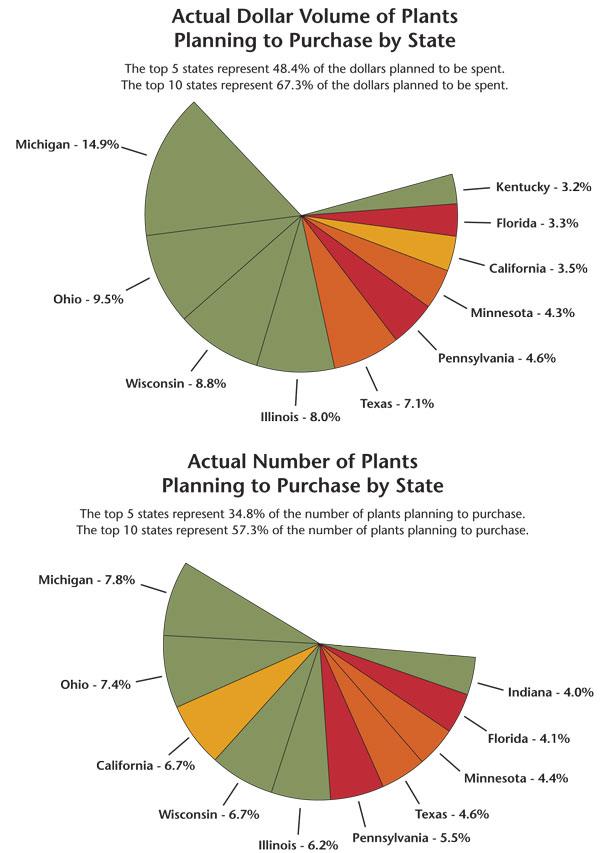

Not only has spending increased substantially at these larger (but not the largest) plants, but the dollars spent has also become more concentrated. The Midwest always has been a metal fabrication center, and it’s becoming even more so.

Rounding out the top five states are Michigan, Ohio, Wisconsin, Illinois, and Texas—no surprises there. What is somewhat surprising is just how much equipment spending is expected to occur in these states. Metal fabrication plants in these top five states make up 48.4 percent of total projected spending for the entire country. That’s a higher geographic concentration of spending than projected in any FMA capital spending survey in the past seven years. Still, while equipment spending in pure dollar terms has become more geographically concentrated, actual metal fabrication plants have become less concentrated. In 2007 a little less than 40 percent of all metal fabrication plants in the survey were in just five states. Today that number has decreased to 34.8 percent (see Figure 2).

All this may imply several significant shifts in the industry landscape. First, when it comes to capital spending—both in terms of dollars spent and number of metal fabrication plants—Michigan is ruling the roost, perhaps a testament to the automotive industry’s resurgence.

Second, operations that are spending the most are concentrated in fewer states. After the recession, stronger players have grown in these markets while the weaker players have fallen away. Today a local market may have fewer metal fabrication plants, but collectively they’re spending more. Consider Michigan again. The state has only 7.8 percent of all metal fabrication plants in the study, but they account for almost 15 percent of all dollars spent on capital equipment nationwide.

Third, capital spending growth is concentrated at small companies and at larger operations—but not at the largest operations. This may hint at an outsourcing trend, with large OEMs outsourcing more metal fabrication work to reliable, top-performing contract fabricators. Larger top performers may have the scale and capacity to satisfy demand, while the smallest top performers can quickly turn around low volumes of specialized work.

As always, welding power sources top the list, but what comes after that gets intriguing. Fabricators expect to spend more than $224 million on laser cutting systems, the largest amount in six years. So is the amount for turret punch press spending, up almost 25 percent over last year’s forecast. Plasma cutting machine spending is projected to be more than 40 percent higher than last year, and projected waterjet machine spending is up nearly 20 percent. Of all spending on primary cutting equipment, only oxyfuel cutting is down from last year (see Figure 3).

Percentagewise, the greatest increase is for servo presses, with spending levels projected to be well more than triple what they were last year. That’s still much less than the projected spending for traditional mechanical presses—a much more mature market, obviously—but it’s still a jump worth noting.

Overall spending projections increased only 4 percent over last year, so some massive gains were offset by declines in other categories, hydraulic press brakes among them. Still, 2013 projections for press brakes are higher than they were two years ago.

Most significant is that after falling by almost 50 percent during the recession, total projected spending has bounced back almost to its pre-recession high. There’s barely a 1 percent difference. Just imagine if the overall economy had such resilience. If it did, the presidential election season would have been entirely different.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}

{kind=link}

{kind=link}